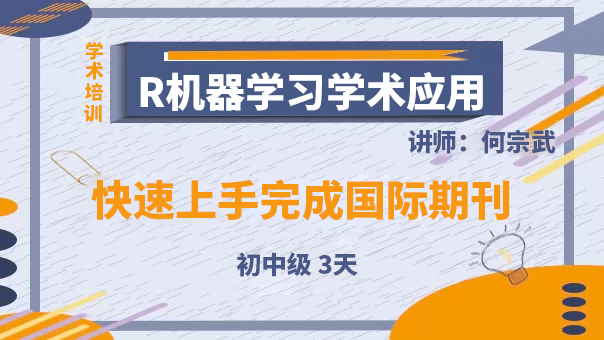

上课信息

上课时间:

2020年8月10-12日(三天)

9:00-12:00, 14:00-17:00, 答疑

上课地点: 远程直播,提供录播回放

Theory: Features of time series data and forecasting basics

R Lab: time series objects (libraries of timeSeries, xts, & mFilters)

Statistical Learning (SL):

(0.5 Hour) One-step forecasting: one-step ahead model fit

(0.5 Hour) Multi-step forecasting: recursive and direct methods

(6 Hours) Linear models: ARIMAs, ETS, BATS, GAMS, Bagged; 案例实做与写作范例

(5 hours) Nonlinear models: Neural Network, Smooth Transition, and AAR; 案例实做与写作范例

R Lab: libraries of forecast, tyDyn, vars, and MSVAR.

Research Issues: unemployment forecasting, predictability of exchange rates and asset returns.

| 报名时间 | 2020-05-25 00:00 至 2020-08-09 00:00 |

|---|---|

| 培训时间 | 2020年8月10-12日(三天) |

| 培训地点 | 远程直播,提供录播回放 |

| 培训费用 | 3000元/2600元(学生优惠价仅限全日制本科及硕士在读),食宿费用自理 |

| 授课安排 | 9:00-12:00, 14:00-17:00, 答疑 |

讲师介绍:

何宗武教授,美国University of Utah经济学博士,现为台湾师范大学管理学院教授。专长为资产订价,总体计量,和融合经济计量方法和机器学习的计量数据科学 (Econometric Data Science)。何教授曾在同济大学经济与金融学院担任暑期客座高等计量方法讲席,2019年将多年讲稿由机械工业出版为经济与金融计量方法,综合著作有7本计量经济和大数据解析的专书。

有近30篇发布在优良的国际期刊,如J. of Applied Statistics, JIMF, JIFM, Empirical Economics, J. ofMacroeconomics等,最近一篇以机器学习方法设计投资组合,已被Journal of Financial Data Science接受,将于2020年6月刊登,此文提出改善投资组合的鸡尾酒算法,在SSRN下载量名列前10%.

课程说明:

因应数字科技时代而备受重视的机器学习方法,核心在于超强的预测能力。而预测这件事也是统计学的重心,统计预测以估计「条件期望值」(conditional mean)为重心,机器学习则透过分类算法直接追踪数据特征。目前机器学习方法涉入的领域十分庞大,时间序列是一个值得多加注意的领域。主要是因为时间序列的序列相关特性(serial correlations),让训练这件事的抽样过程要一段段设计,必须十分小心。

本课程针对「如何执行机器学习的时间序列预测」,关键领域是经济与财务实证上的预测性(Predictability),议题包括,资产报酬率和汇率变动的预测性,失业率预测,波动预测(volatility forecasting)以及机器学习之因果检测(Machine learning Granger causality)。这些议题在财经学术文献上皆有一定的地位,若能以机器学习的方法提出贡献,研究成果必受肯定。

本课程实做部份,皆会以一份期刊文献关键论文(key paper)为基准,以程序代码说明与对照实证文献上的重点,然后针对机器学习的可延伸贡献出做出对照结果;更重要的是,课程会针对特定议题,提供word的英文写作模板,学习者研习之后,将可以很快上手,完成一篇以国际期刊为目标的研究大纲。

学员背景:

为利于掌握机器学习的预测架构,本课程不适合统计零基础的学员,参与学员必须具备进中级应用统计(Intermediateapplied statistics)或计量经济学(Applied Econometrics)的基础,本科硕士程度不限。

有程序语言的逻辑会更好,但非必要,课程会做R手把手教学(Hands-on tutorials)。

优惠:

现场班老学员9折优惠;

同一单位三人以上同时报名9折优惠;

同一单位六人以上同时报名8折优惠;

以上优惠不叠加。

联系方式:

尹老师

电话:010-53352991

QQ:42884447

WeChat:yinyinan888

参考文献:

Ahmed, N. K., Atiya, A.F., Gayar, N. E., & El-Shishiny, H. (2010). An empirical comparison ofmachine learning models for time series forecasting. Econometric Reviews, 29(5-6), 594-621.

Bergmeir, C., Hyndman,R. J., & Benítez, J. M. (2016). Bagging exponential smoothing methods usingSTL decomposition and Box–Cox transformation. International Journal of Forecasting, 32(2), 303-312.

a) Chakraborty, C., &Joseph, A. (2017). Machine learning at central banks. Staff working paper No.674, Bank of England.

Chevillon, G (2007) Direct multi-stepestimation and forecasting. Journal ofEconomic Surveys, 21(4), pp. 746–785.

Clements, M and D Hendry (1998). Forecasting Economic Time Series.Forecasting economic time series. Cambridge University Press.

Cochrane John H. (2008)The Dog That Did Not Bark: A Defense of Return Predictability. Review of Financial Studies, 21(4),1532-1575.

De Livera, A. M.,Hyndman, R. J., & Snyder, R. D. (2011). Forecasting time series withcomplex seasonal patterns using exponential smoothing. Journal of the American Statistical Association, 106(496),1513-1527.

De Stefani, J., Caelen,O., Hattab, D., & Bontempi, G. (2017). Machine learning for multi-stepahead forecasting of volatility proxies. In MIDAS@ PKDD/ECML,17-28.

Edlund Per-Olov and Karlsson S. (1993)Forecasting the Swedish Unemployment Rate: VAR us. Transfer Function Modelling.International Journal of Forecasting,9(1), pp. 61-76.

Feng, L., & Zhang,J. (2014). Application of artificial neural networks in tendency forecasting ofeconomic growth. Economic Modelling,40, 76-80.

Franses, P. H., & Van Dijk, D. (2000). Non-linear Time Series Models in EmpiricalFinance, Cambridge University Press.

Gogas, P., Papadimitriou, T., Matthaiou, M.,& Chrysanthidou, E. (2015). Yield curve and recession forecasting in amachine learning framework. ComputationalEconomics, 45(4), 635-645.

Hafezi, R., Shahrabi, J., & Hadavandi, E.(2015). A BAT-Neutral network multi-agent system (BNNMAS) for stock priceprediction: Case study of DAX stock price. AppliedSoft Computing, 29, 196-210.

Hall Aaron Smalter (2018) Machine LearningApproaches to Macroeconomic Forecasting. EconomicReview, Federal Reserve Bank of Kansas, Available at: https://www.kansascityfed.org/~/media/files/publicat/econrev/econrevarchive/2018/4q18smalterhall.pdf

Hamzaçebi, C., Akay, D., & Kutay, F. (2009).Comparison of direct and iterative artificial neural network forecastapproaches in multi-periodic time series forecasting. Expert Systems with Applications, 36(2), 3839-3844.

Ho, Tsung-Wu (2019) Machine Learning is notas Good as you Think for Time Series Forecasting: Evidence from MultistepForecasting. Available at: https://ssrn.com/abstract=3496138.

Ho, Tsung-Wu (2020) Portfolio Selection usingportfolio committees. Forthcoming in theJournal of Financial Data Science.

Hyndman, R. J. and Athanasopoulos, G. (2018). Forecasting: principles and practice.2nd edition, OTexts.com/fpp2.

Lewellen Jonathan (2004) Predicting returnswith financial ratios. Journal of FinancialEconomics, 74, 209–235.

Montgomery, Alan L, Victo Zarnowitz, Ruey S.Tsay, and George C. Tiao (1998) Forecasting the U.S. Unemployment Rate. Journal of the American StatisticalAssociation, 93(442), pp. 478-493.

Patel, J., Shah, S., Thakkar, P., & Kotecha,K. (2015). Predicting stock market index using fusion of machine learningtechniques. Expert Systems with Applications, 42(4), 2162-2172.

Rothman Philip (1998) Forecasting AsymmetricUnemployment rates. Review of Economicsand Statistics, 80(1), pp.164-168.

Saad, E., Prokhorov, D., and Wunsch, D.(1998) Comparative study of stock trend prediction using time delay, recurrentand probabilistic neural networks. IEEETransactions on Neural Networks 9(6), pp. 1456–1470.

Serinaldi, F. (2011). Distributional modelingand short-term forecasting of electricity prices by generalized additive modelsfor location, scale and shape. Energy Economics, 33(6), 1216-1226.

Sorjamaa, A, J Hao, N Reyhani, Y Ji, and ALendasse (2007). Methodology for long-term prediction of time series. Neurocomputing,70(16), pp. 2861–2869.

Tasci, Murat (2012) Ins and Outs ofUnemployment in the Long-Run: Unemployment Flows and the Natural Rate. Working Paper #12-24, Federal ReserveBank of Cleveland.

Taylor, J. W. (2003). Short-term electricitydemand forecasting using double seasonal exponential smoothing. Journal of the Operational Research,54(8), 799-805.

Torres, J. F., Galicia, A., Troncoso, A., &Martínez-álvarez, F. (2018). A scalable approach based on deep learning for bigdata time series forecasting. IntegratedComputer-Aided Engineering, 25(4), 335-348.

ülke, V., Sahin, A., & Subasi, A. (2018). Acomparison of time series and machine learning models for inflationforecasting: empirical evidence from the USA. Neural Computing and Applications, 30(5), 1519-1527.

Vapnik V. (2000) TheNature of Statistical Learning Theory, 2nd. Springer-Verlag, NewYork.

Wood, S. N., & Augustin, N. H. (2002). GAMswith integrated model selection using penalized regression splines andapplications to environmental modelling. Ecologicalmodelling, 157(2-3), 157-177.

Zhang, G., & Hu, M. Y. (1998). Neuralnetwork forecasting of the British pound/US dollar exchange rate. Omega, 26(4), 495-506.

Zhao, Y., Li, J., & Yu, L. (2017b). A deeplearning ensemble approach for crude oil price forecasting. Energy Economics, 66, 9-16.

Zhao, Z., Chen, W., Wu, X., Chen, P. C., &Liu, J. (2017a). LSTM network: a deep learning approach for short-term trafficforecast. IET Intelligent Transport Systems, 11(2), 68-75.

顾问微信

顾问微信

©2026Peixun.net 北京国富如荷网络科技有限公司 版权所有 未经许可 请勿转载

京ICP备11001960号-4

京公网安备 11010802034634号

京公网安备 11010802034634号

邮件已发送!

已成功发送邮件到您注册的邮箱 请前往查询并点击链接重置密码

分享

分享 收藏

收藏

扫码二维码

扫码二维码